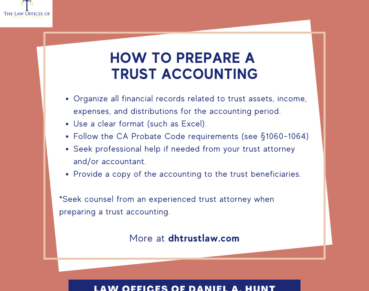

How to Keep Records as a Trustee

If you’re serving as the trustee of a trust, you need to know the right way to keep financial records. Annually, you will need to account to the present beneficiaries of the trust for all money that came into and went out of the trust.

If at the end of the accounting, the money doesn’t add up properly, you may be required to reimburse the trust for those funds out of your own pocket, out of your trustee fee, or out of your beneficial share of the estate.

We’re going to help you avoid this error by sharing 3 steps to keeping records as a trustee.

Step 1: Collect Financial Statements

First, obtain a statement from each financial institution to find the starting balance for each account.

If you are a successor trustee over a trust where the Settlor has died, you will use the account balance on the date of the settlor’s death as the starting balance.

If you’re taking over as acting trustee for a trust where the settlor has resigned or been declared incapacitated, you will use the date of your appointment in that role as the starting balance.

Step 2: Create a Ledger

There are 3 main options when it comes to creating a ledger.

- Use a handwritten ledger

- Use a paid accounting software program (such as QuickBooks)

- Use a simple spreadsheet system (such as Microsoft Excel or Google Sheets)

Of these three methods, no particular method is necessarily superior; it’s mostly a matter of the trustee’s personal preference. However, you may want to check with the estate planning firm who will be preparing the trust accounting and inquire as to their preference before you begin.

Step 3: Keep scrupulous records of all transactions

A trustee must keep careful records of all transfers of money and property into or out of the trust. Track all disbursements and transactions. Document the decision-making process for all trust investments.

Your records must account for:

- The nature and value of the trust assets when received.

- How much principal and income the trust has received and from where.

- How much principal and income has been disbursed and to whom.

- Any commissions paid.

- The amount and location of any balance on hand.

- Expenditures, gains, or losses of the trust.

Be sure to keep your personal funds separate from the trust’s funds. Never commingle personal and trust funds. Doing so could confuse your records and create the appearance of stealing money from the Trust.

How long to keep records

Keep copies of any relevant vouchers, receipts, and other documentation of disbursements, expenses, and capital transactions. If a beneficiary ever raises questions about the accounting, this evidence will come in handy.

One of the last tasks in a trust administration is filing a final tax return. Ask the CPA who assists you for advice on how long to keep trust administration records. Before throwing out any paperwork, you’ll want to be sure that the IRS won’t be auditing the fiduciary returns. Usually, three years is sufficient, but a period of up to seven years may be advised.

Two Costly Record-Keeping Mistakes

Here’s a cautionary tale that illustrates the importance of keeping accurate records. One of our clients, whom we’ll call John White, failed to keep accurate records while acting as a trustee. At the end of the accounting year, it was time to prepare an accounting. He tried to piece together what had happened to the trust funds, but his numbers didn’t add up properly.

Because of the discrepancy in trust funds, John had to reimburse the trust over $30,000 out of his trustee fee and beneficial share! For John, poor record-keeping was a costly mistake.

Not correcting an imbalance in trust funds can be another expensive mistake. If the beneficiaries see a deficit in the trust accounting, they may threaten to sue you for breach of your fiduciary duties. Did you know that trust litigation often costs tens of thousands of dollars? Keeping fastidious records can be labor-intensive, but it’s well worth the time and effort because of the dangers you’ll avoid by doing so.

For detailed counsel on how to keep accurate records as a trustee (and limit your potential for getting sued by a beneficiary), feel free to contact our office.

Law Offices of Daniel A. Hunt

The Law Offices of Daniel A. Hunt is a California law firm specializing in Estate Planning; Trust Administration & Litigation; Probate; and Conservatorships. We've helped over 10,000 clients find peace of mind. We serve clients throughout the greater Sacramento region and the state of California.

Related posts

More From Daniel Hunt Law

- Trust Administration

- Trust Administration

- Trust Administration